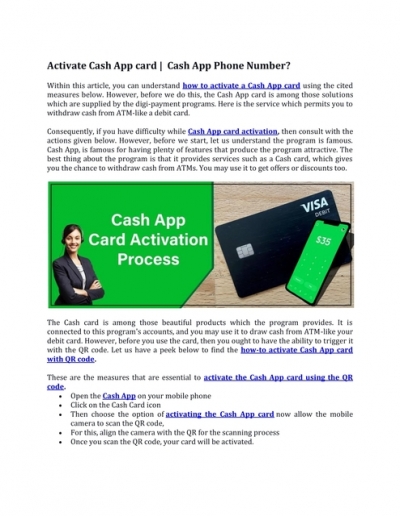

As long as you create money to the-date, an effective HELOC usually generally speaking not damage the credit. Whilst you will receive a painful inquiry added to your own borrowing statement once you make an application for the HELOC, the effects of the are usually quick-term. Individuals with a strong borrowing from the bank reputation will most likely not actually come across a beneficial procedure effect in the tough inquiry.

Probably one of the most visible ways a good HELOC is hurt their borrowing from the bank is when your miss a repayment. Like with any other kind regarding mortgage, forgotten a good HELOC commission will result in a good derogatory mark-on your credit score. Derogatory marks you are going to significantly ount of your time, therefore it is crucial that you create your month-to-month HELOC payments on time along with complete.

Indeed there ifications when you have slim borrowing from the bank profiles when they personal their HELOC. In case the HELOC is the most just a couple of membership on your own credit history, there is certainly a chance your credit history could well be inspired t when you intimate it. Individuals who just have an effective HELOC could see the get just take a bump when they close-out its membership.

To get rid of a derogatory mark on your credit, make sure to do not skip a payment. Having several other credit lines discover over time may help you stop a possible credit history miss after you close your HELOC. Analogy lines of credit can sometimes include credit cards, automobile financing, college loans, otherwise home financing.

Unfortunately, continue reading this there isn’t far you could do to store a hard inquiry away from affecting your own borrowing but with a robust credit character before your pertain could help. Although not, the results regarding a hard query could be beat with responsible borrowing from the bank fool around with, such as making payments punctually and you may avoiding a top borrowing from the bank utilization, so you should not let the prospective bad influences of a difficult query stop you from using if you believe a HELOC is the best selection for your.

HELOC choice

![]()

Regardless of if HELOCs was a great way to borrow on your own home’s equity, they’re not for everybody. Several choices allow you to acquire using your home’s collateral since security, such household collateral funds and cash aside refinances.

Domestic collateral loan

House guarantee finance was another great cure for tap into the fresh collateral accumulated of your property. Instance HELOCs, domestic equity finance is actually a type of next mortgage. Although not, home guarantee fund have a tendency to come with fixed rates, to help you trust a predictable monthly payment each month. An alternative huge difference is the fact home security money render a lump sum payment instead of a personal line of credit. Like with a great HELOC, you need the bucks in the loan for all you require, out-of a vacation in renovations.

Cash-out refinance

Cash out refinances try a fairly underutilized way to remove guarantee out of your home. That neat thing in the a cash out refinance would be the fact they you will streamline your current mortgage repayment and cash lent out of your collateral toward one monthly payment.

Cash-out refinances range from a timeless rates and you can title re-finance in the way which you borrow more the degree of your current home loan, toward differences coming to you for the bucks. That it refinance choice shall be including useful when newest interest rates are lower than your current home loan or for those who have viewed the degree of security found in your house improve throughout the years.

Closing view: So how exactly does HELOCs connect with your credit score?

In the event HELOCs can impact your credit score, that doesn’t indicate its impression will be damaging full. As long as you borrow responsibly and work out costs on time, your own HELOC could help reinforce your rating and may also actually improve they over time. In the event the a HELOC doesn’t look like the best choice, think a property collateral mortgage or cash-out refinance since the alternatives to possess tapping into your house guarantee.